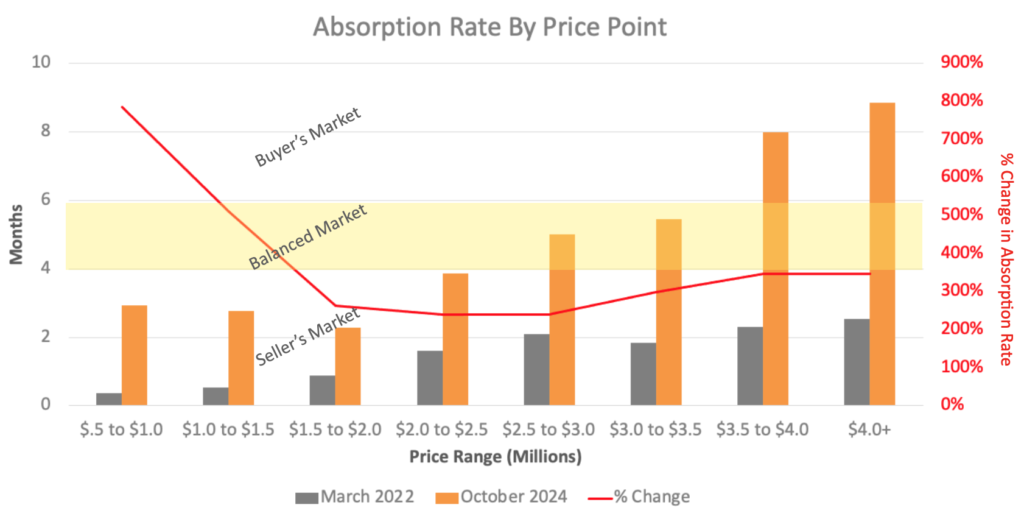

Since March 2022, the Federal Reserve has raised interest rates 11 times, increasing the cost of a 30-year fixed-rate mortgage from 3.75% to 6.80% (Federal Reserve Economic Data). To understand the impact of these rate hikes on the Denver market, we analyzed the absorption rate across increasing price ranges to see how the competitive landscape has shifted.

The absorption rate is a key measurement of market competitiveness, representing the balance of supply and demand. It calculates the months required to sell the current inventory of homes for sale based on the sales rate over the previous 12 months. The orange bars below show across all price ranges that the absorption rate is much slower today than before the interest rate hikes commenced, as shown by the gray bars.

The red line shows the percentage change in the absorption rate due to interest rate hikes at each price range. Not surprisingly, higher interest rates have a strong chilling effect on the market in the $500,000 to $1 million range. However, even the $4 million plus higher-end market is not entirely immune.

According to the National Association of Realtors, a balanced market is about four to six months of supply, the yellow band. Anything below that is considered a seller’s market; above it, a buyer’s market. As our chart shows, recent rate increases have moved homes priced between $2.5M and $3.5M into a balanced market, while homes over $3.5M have entered a buyer’s market.

Higher interest rates impact the lower-end market more significantly. Yet, despite this change, the lower-end market remains a seller’s market, albeit less so. Meanwhile, the higher-end market has been less affected, yet enough to shift it to either a balanced or buyer’s market.